Remote Work and the Allocation of Taxation Rights over Corporate Income

About the project

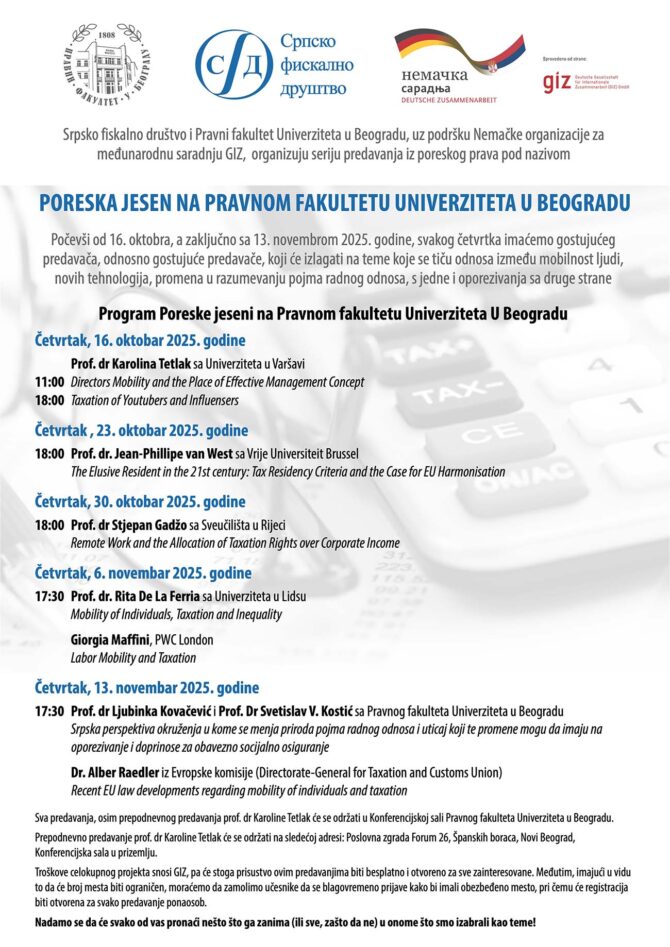

The Fourth Lecture, 30 October 2025

Speaker: Prof. Dr Stjepan Gadžo, Faculty of Law, University of Rijeka (Croatia)

The growing cross-border mobility of individuals and the rise of various remote work arrangements are challenging the time-honoured foundations of international tax law. Based on existing understanding of the permanent establishment (PE) concept in the international tax law, this lecture examined the key implications of the remote and hybrid work for the allocation of taxing rights over corporate income, with particular emphasis on the changes in the interpretation of PE and amendments to OECD Commentary. Prof. dr Gadžo further presented a comparative analysis of views of different countries on the elements affecting the creation of PE, suggesting that new, objective criteria should be introduced in future international tax guidelines.

Share